Overture Orthopaedics has surpassed $1.0 million in sales of its OvertureTi Knee Resurfacing System, a 510(k)-cleared implant designed to address articular cartilage lesions and early-stage osteoarthritis in patients considered too young or unsuitable for full arthroplasty. The announcement highlights growing commercial traction for an implant that positions itself as a cost-effective, surgically streamlined alternative to biologic repair strategies

Why this milestone points to a deeper clinical shift in knee preservation strategy

The sales achievement, while modest in absolute terms, reflects early momentum for a product situated in one of the more complex clinical gray zones in orthopaedic care—patients aged 35 to 65 with symptomatic cartilage lesions or early degenerative joint changes who are deemed poor candidates for total knee arthroplasty. This population is expanding, fueled by more active aging cohorts and rising sports-related injuries in mid-life.

Overture Orthopaedics’ success with the OvertureTi system signals growing surgeon willingness to explore partial resurfacing options where biologic strategies often underperform and where patients resist the finality of total joint reconstruction. While $1 million in sales does not imply wide adoption, it suggests commercial validation for a market thesis built around hybrid hardware-biologic preservation that delays progression to full replacement.

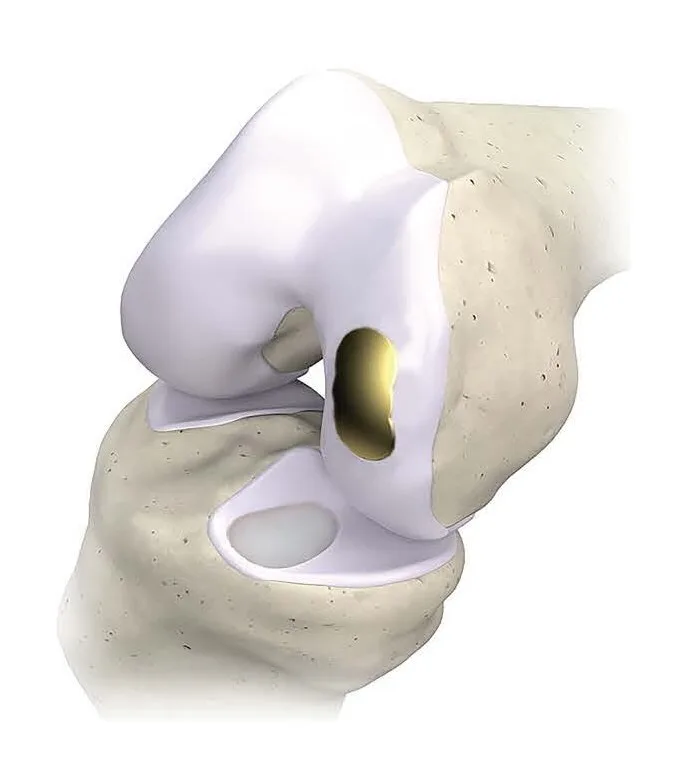

The procedure, described as “Focalplasty,” replaces only diseased sections of the joint using 3D printed titanium and Vitamin E–treated polyethylene components. The design focuses on anatomical preservation and localized intervention—an approach increasingly attractive as biologic treatments face headwinds around cost, complexity, and durability.

What this reveals about the evolving gap between biologic repair and arthroplasty

Several high-cost biologic repair strategies—such as autologous chondrocyte implantation (ACI), osteochondral allografts, and matrix-induced autologous chondrocyte implantation (MACI)—continue to dominate the therapeutic window for patients with early cartilage degradation. However, these techniques come with trade-offs. Industry observers note concerns over healing variability, donor site morbidity, long recovery timelines, and high procedural cost. ACI, for example, may exceed $80,000 per episode of care when factoring in multi-stage surgeries and lab processing.

In contrast, Overture’s system presents itself as a mechanically straightforward, single-procedure alternative that forgoes biologic regeneration in favor of durable, inert surface replacement. While this forfeits the theoretical regenerative upside of biologics, it gains ground by offering more predictable timelines and clearer surgical endpoints. According to orthopaedic surgeons tracking joint preservation modalities, the adoption of implants like OvertureTi reflects growing pragmatism among both providers and patients about what mid-life knees need most—stability, pain relief, and surgical clarity, not necessarily cellular regeneration.

How this platform navigates the regulatory and scalability landscape

The OvertureTi Knee Resurfacing System is cleared under the U.S. Food and Drug Administration’s 510(k) pathway, placing it in the same regulatory tier as most traditional orthopaedic implants. The system includes pre-sterilized, single-use instrumentation—a feature designed to streamline adoption in ambulatory surgical centers (ASCs) and hospital operating rooms by reducing sterilization turnaround and logistical burden.

From a scalability standpoint, the use of 3D-printed titanium and standardized implant geometries aligns well with distributed manufacturing and inventory strategies. While more complex biologic therapies may face site-specific training and processing constraints, implants like OvertureTi are inherently easier to train on, distribute, and scale within a value-conscious provider network.

That said, reimbursement pathways may remain less defined for procedures that don’t map neatly to existing DRGs or CPT codes associated with full or partial arthroplasty. Health insurers may push back on newer implant codes without long-term data, especially for patient populations that still fall into a grey reimbursement zone between conservative management and joint replacement.

What risks and clinical questions still surround focal resurfacing as a category

While promising, focal metallic resurfacing is not without limitations. Surgeons and payers alike are watching for long-term data around wear rates, implant integration, and downstream surgical complexity. Industry observers have raised questions about how these implants behave under load over 5–10 years, and whether partial metallic surfaces create revision challenges later when full arthroplasty becomes necessary.

Additionally, adoption could be limited by surgical inertia. Many orthopaedic surgeons remain trained predominantly on either biologics or full replacement workflows, and may not feel comfortable embracing a mid-spectrum intervention. Procedural billing complexity and questions around optimal patient selection criteria could further slow mainstream integration.

Overture Orthopaedics must also navigate market education. The company’s Focalplasty positioning may resonate with high-volume sports medicine surgeons, but will need broader orthopedic buy-in to generate procedural critical mass. A deeper KOL network and expanded data sets will likely be necessary to penetrate beyond early adopters.

Why timing and positioning could give Overture a commercial edge in 2026

Despite these challenges, the commercial timing may be fortuitous. Biologic cartilage repair procedures are increasingly facing payer scrutiny due to cost and inconsistent outcomes, while younger patient populations are increasingly rejecting joint replacement as a first solution. The desire for “joint preservation” has matured from a vague ideal into a surgical category with real hardware—and real sales milestones.

By planting its flag firmly in this transition zone, Overture Orthopaedics is attempting to create not just a product, but a category-defining platform. Whether this evolves into a standalone standard of care or remains a niche segment will depend heavily on surgeon training, patient education, and reimbursement integration in 2026 and beyond.

For now, the $1.0 million sales mark—while early—is a signal that payers and patients are at least beginning to respond to that message.

To sustain momentum, Overture Orthopaedics may also need to invest in longitudinal outcomes research and registry participation to validate implant durability over time. As more procedures shift to outpatient settings, especially within ASCs prioritizing efficiency and bundled payments, Overture’s pre-packaged, sterilized system design could offer operational advantages. However, long-term success will depend not just on device performance, but on whether the procedure can carve out procedural standardization and payer alignment in a market where mid-stage joint interventions often fall through the reimbursement cracks.

Overture’s titanium implant sees rising use in patients too young for total knee replacement added by Pallavi Madhiraju on

View all posts by Pallavi Madhiraju →