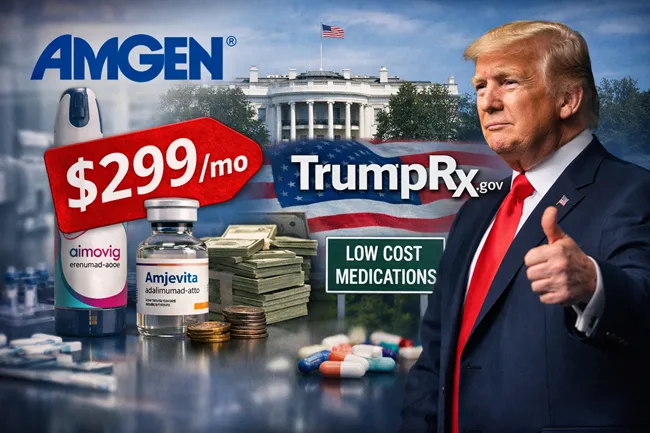

Amgen has expanded its direct-to-patient program, AmgenNow, to include Aimovig (erenumab-aooe) and Amjevita (adalimumab-atto), each now available at a flat monthly price of $299 for eligible U.S. patients. This development forms part of Amgen’s broader agreement with the Trump Administration, satisfying conditions laid out in the President’s July 31 policy letter and positioning the company for tariff relief through alignment with Most Favored Nation pricing benchmarks. Both therapies will also be offered on TrumpRx.gov, joining Repatha (evolocumab), which was discounted in October 2025.

What this reveals about biopharma’s evolving strategy to navigate federal pricing mandates

Amgen’s latest announcement is not simply a gesture of goodwill or a marketing tactic. It reflects a calculated, policy-aligned maneuver in an increasingly high-stakes environment where biopharmaceutical companies are being pushed to publicly demonstrate pricing restraint. The Trump Administration’s Most Favored Nation pricing push, while politically controversial, has catalyzed a new framework of compliance that is being negotiated outside traditional legislative mechanisms. In this context, Amgen’s expanded participation in TrumpRx.gov signals a strategic attempt to protect pricing autonomy in commercial and Medicare segments while offering targeted relief to cash-paying patients.

This shift may represent a larger strategic realignment across the pharmaceutical sector. Rather than contesting pricing reform through lobbying or litigation, some companies appear to be embracing a hybrid approach—granting symbolic concessions to secure longer-term policy insulation. Industry analysts note that TrumpRx.gov, while still in its early stages, is rapidly becoming a new proving ground for pricing optics and government relations, with Amgen now emerging as one of its most prominent early adopters.

What changes for biologic access and biosimilar positioning under direct-to-patient models

The addition of Aimovig and Amjevita to AmgenNow substantially expands the company’s direct-to-patient footprint. Aimovig, used for migraine prevention, and Amjevita, Amgen’s biosimilar to AbbVie Inc.’s blockbuster Humira, are now both being marketed to eligible American patients at a flat monthly cost that bypasses insurance. The price cuts are substantial. For Aimovig, the $299 figure represents a reduction of nearly 60 percent from its traditional list price. For Amjevita, the discount reaches approximately 80 percent.

However, the impact on access remains conditional. These pricing models are cash-based and require patients to opt into Amgen’s own fulfillment channels or TrumpRx.gov. While this route may appeal to those without insurance or those on high-deductible plans, it does not influence formulary coverage decisions, nor does it guarantee broader adoption through traditional payers or pharmacy benefit managers. The real-world utility of such programs may be limited by logistical friction, digital literacy gaps, and patient preferences.

Yet the move could carry strategic weight in terms of competitive positioning. For Amjevita, undercutting other biosimilars in the same class via a direct-cash channel creates a new pricing floor that may alter both market dynamics and payer negotiations. For Aimovig, the discount could put pressure on anti-CGRP rivals like Eli Lilly and Company’s Emgality or AbbVie Inc.’s Qulipta, particularly if the TrumpRx platform gains consumer traction.

Clinicians tracking the migraine space note that this shift may benefit a subset of patients unable to secure coverage or deal with prior authorization delays. But they also caution that clinical uptake will depend on sustained affordability, program visibility, and clarity around medical support services, including patient education and follow-up. Ultimately, the question is whether this retail-style pricing approach will remain a niche access channel or begin to displace parts of the conventional reimbursement framework.

Why Amgen’s U.S. manufacturing investments matter beyond capacity

The pricing and policy components of this announcement were accompanied by fresh investment disclosures. Amgen stated it will invest an additional $2.5 billion in U.S. manufacturing operations, including $900 million in Ohio and $1 billion in North Carolina. These figures build on the more than $40 billion the company has invested since 2018 in domestic research and production. These investments were originally catalyzed by the Tax Cuts and Jobs Act of 2017 and are now being reinforced under the 2025 One Big Beautiful Bill Act, which incentivizes pharmaceutical onshoring through tax and trade policy.

In return, Amgen will receive relief from industry-specific tariffs for a period of three years. The structure of this benefit has not been publicly detailed, but policy watchers believe it reflects a new regulatory contract. Under this model, U.S.-based manufacturing and visible patient-facing discounts act as leverage for exemption from future pricing scrutiny or trade penalties. For Amgen, this tariff relief could protect its margin structure on certain imported intermediates or components used in biologic manufacturing.

This approach also serves a political function. By tying U.S. pricing concessions to job creation and manufacturing infrastructure, Amgen strengthens its positioning in a volatile policy environment. Other firms that have pursued more confrontational strategies on pricing may find themselves without equivalent levers of influence. If the TrumpRx model is adopted more broadly, capital investment could become a prerequisite for regulatory goodwill in ways that fundamentally reshape the cost-benefit calculus of domestic versus offshore production.

What the TrumpRx shift implies for future pricing regulation enforcement

While Amgen’s participation in TrumpRx.gov may currently appear optional, its growing institutionalization could evolve into a baseline requirement for operating within the U.S. market. For now, the platform functions as an opt-in program for companies seeking to demonstrate alignment with federal pricing goals without directly altering their net prices across broader distribution channels. But this segmentation—public discounting alongside private price maintenance—may not withstand long-term regulatory scrutiny.

There is a real possibility that future administrations or congressional oversight committees will reevaluate whether participation in such programs constitutes adequate compliance under the Inflation Reduction Act or future legislation. If TrumpRx.gov scales rapidly and proves effective at delivering visible affordability improvements, it may also become politically attractive to expand its scope or enforce participation across additional classes of drugs.

Additionally, the blurred line between retail programs and government platforms raises unresolved questions about liability, data handling, and rebate obligations. If more biopharma companies follow Amgen’s lead, regulators may demand standardization around eligibility, distribution, and reporting. In the meantime, investors and institutional buyers will be watching closely for signs of erosion in average selling prices, net margins, or payer relationships as these parallel programs expand.

For Amgen, this moment signals tactical success. The company has sidestepped confrontational pricing reform with a move that supports patients, builds goodwill, and deflects policy risk. But that success is predicated on a narrow channel. Whether that channel remains an exception or becomes the rule is now a question for the rest of the industry.